Hale "Bondad" Srewart

Ever since I have been writing about the economy (about 4 years) I have focused on the mammoth increase in US debt during this expansion. It has led me to question the underlying vitality of this expansion as a whole. Events of the last six months indicate the markets are also asking the same question right now, although in a somewhat different way.

In effect, the economic dominoes are starting to fall. Ultra-low interest rates which inflated asset prices and allowed an explosion of debt are starting to seriously bite as a financial system is burdened with too much bad debt on its books. In addition, the market is starting to realize that asset prices -- namely housing -- were ephemeral and will have to drop. In effect, the entire economy is going through a process of reevaluating "the greatest story never told" and are discovering it wasn't that good a deal to begin with.

Let's start with a few basic charts.

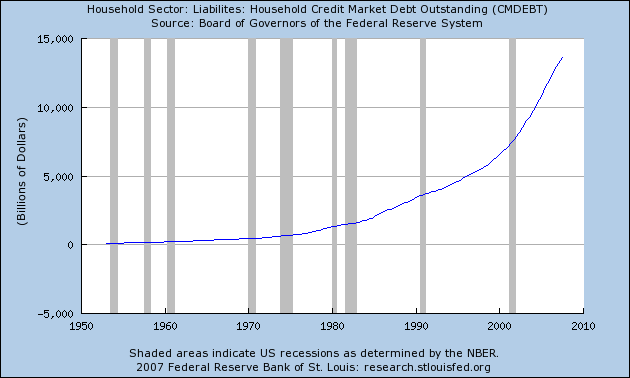

Above is a chart from of total household debt. Notice the curve is almost parabolic over the last few years -- and especially this expansion.

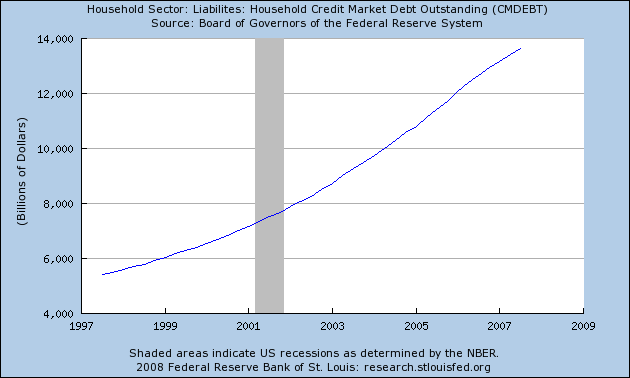

Above is a 10 year chart of household debt. Notice it has increased from about $8 trillion to a little under $14 trillion, which is a really big increase.

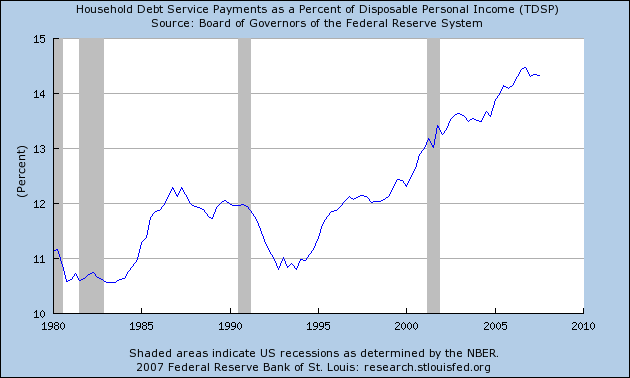

As a result of this increase in total household debt outstanding, the household debt payment ratio has increased to the highest level in 25 years.

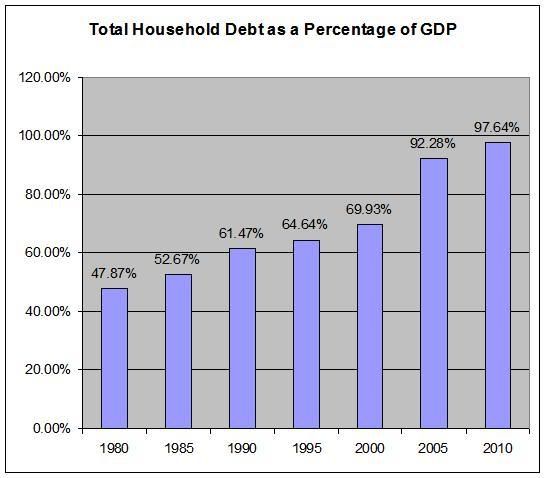

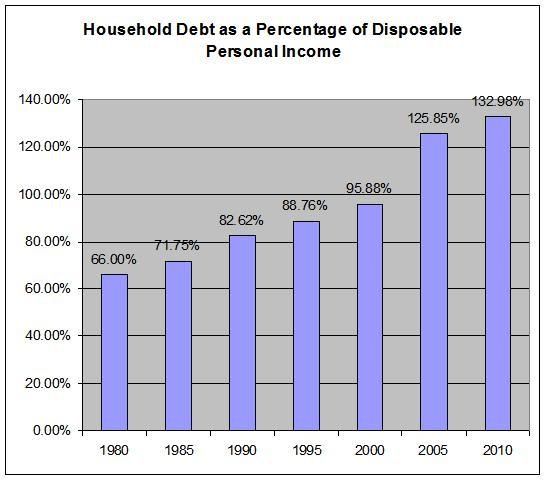

Let's place the household debt level in perspective. Here is a chart tabulated every 5 years of total household debt outstanding and its percentage of GDP and total disposable income. The GDP and disposable income numbers are from the Bureau of Economic Analysis and the household debt numbers are from the Federal Reserve's Flow of Funds Report. The figures for 2007 are for the third quarter.

Notice that both percentages jumped sharply during this expansion. This is what easy credit will do for you.

Now -- this massive debt orgy has allowed the US to inflate its home prices.

This has allowed Americans to extract home equity loans from their homes to buy more stuff. Because home prices increased so much in value, Americans felt richer, so they felt as though they could spend more.

Now, I'm not alone in questioning this expansion. Business Week has an article titled, How Real Was the Prosperity?" where they ask the same question.

Consumer Spending: The rule for a prudent individual is simple: Don't spend more than you make. For a long time, the U.S. economy obeyed that rule. As far back as the 1960s, personal spending, adjusted for inflation, has basically tracked the overall growth of the economy, as measured by gross domestic product. Sometimes consumers would get ahead of the economy for a few years, and sometimes fall behind, but never for very long.

That pattern changed in the 1990s. As of the third quarter of 2007, the 10-year growth rate for consumption was 3.6%, vs. GDP growth for the same period of 2.9%. This difference represents an enormous gap. If consumer spending had tracked the overall economy over the past decade as it has in the past, Americans today would be spending about $600 billion less a year. The extra spending has amounted to a total of about $3 trillion since 2001.Consumer Lending. The past 10 years will go down as one of the greatest consumer-lending sprees ever. Adjusted for inflation, consumer debt--including mortgages--rose an average 7.5% per year since 1997, far faster than the 4.2% rate of the previous 10 years. The last time debt rose so fast was the 1960s, as the postwar generation bought homes and autos. If Americans had kept borrowing at their pre-1997 pace, they would have had about $3 trillion less in debt.

Corporate Earnings. Yes, there's been a profit boom in recent years. Corporate earnings, as measured by government statisticians, have averaged 8% of GDP over the past decade, up from a low of 6.5% in the early '90s. That has helped propel stocks upward.

But here's an unfortunate truth--the profit surge has been mainly in one area, financial services. Financial institutions have benefited from the consumer credit boom, the proliferation of new financial instruments, and relatively low rates. By contrast, the earnings of nonfinancial companies over the past decade have averaged about 5.3% of GDP, about the same since the mid-1980s. There are few signs of any acceleration, even after years of restructuring.

Right now we're just starting to deal with the hangover from this debt orgy. The entire financial sector has been wracked by writedowns for the last 6 months. No one has been spared. Estimates are for total writedowns of $300-$500 billion. So far, we've only had $100 billion or so, so we have a ways to go.

We just had the weakest holiday season of the last 5 years, indicating consumers are starting to get tapped out -- they can literally borrow no more. While it is never a good idea to bet against the American consumer who will sell his mother to buy the next thing, high gas and food prices, a tanking housing and stock market and a weakening job market will undoubtedly provide some serious headwinds for the foreseeable future.

Consumer lending is going through the wringer right now as well -- and for good reason. It use to be that all you needed to get a loan was a pulse. Now you actually have to have a credit score.

But the central problem of this expansion is all of that debt has to go somewhere. You can't just slice and dice a pool of debt into many pieces and completely eliminate risk; that just can't be done. But everyone thought you could do it, which is basically how we got into this mess in the first place. Now everyone has the pleasure of choking on a ton of bad loans. And it's not going to stop anytime soon.

To make matters worse, the level of debt in the economy assumes a certain asset value. For example, if a banker makes a $100,000 loan for a $100,000 house and the home starts to decrease in value, the banker will at some time have to write-down the value of the loan. So as home prices decrease anyone who owns mortgage related debt (and that is literally everyone on the planet) will have to write-down the value of their debt. This constrains their ability to make new loans, which hurts an economy like the US which depends on credit creation.

That's the central point to the Business Week article's title. This expansion is based on the inflation of an asset class -- namely, housing. As that asset increased in value, consumers felt wealthier and therefore spent more. They extracted more equity from their homes for more consumer purchases. This was a net positive for consumer spending and the economy as a whole. However, as that asset value decreases -- which is what we are experiencing now -- the exact opposite is also true. Consumers will spend less because they feel less wealthy. And they probably will for some time.

(In accordance with Title 17 U.S.C. Section 107, this material is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. I.U. has no affiliation whatsoever with the originator of this article nor is I.U endorsed or sponsored by the originator.)

The Nazis, Fascists and Communists were political parties before they became enemies of liberty and mass murderers.

No comments:

Post a Comment